In late December 2017, the Tax Cuts and Jobs Act was signed into law marking the biggest tax overhaul in decades. Now that the new year is here and the bill is in effect, small businesses are clamoring to figure out how the changes affect them. Some of the most exciting updates revolve around the expansion of the Section 179 expensing limit and the bonus depreciation reforms.

Section 179

Before we delve into the updates, let’s recap what Section 179 is and how it traditionally helps businesses grow.

The Section 179 Tax Deduction allows a business to deduct the full purchase price of qualifying equipment acquired during that tax year. The deduction often results in thousands of dollars saved the same year it was purchased. This incentive was put into place to motivate small businesses to invest in themselves through equipment.

On January 1st, the changes outlined in the Tax Cuts and Jobs Act officially took effect raising the deduction limit from $500,000 to $1,000,000. The law also increased the spending cap to $2,500,000. With this cap, a company can spend up to $2.5 million before the deduction is reduced. The government imposes these limits on the amount that can be deducted to ensure the incentive is not taken advantage of by large corporations.

Bonus Depreciation

Bonus Depreciation is an additional incentive that is typically used when a business hits the Section 179 deduction cap. It allows for a bonus depreciation of the remaining balance of the purchase. Before the tax reform, bonus depreciation was set to drop from 50% in 2017 to 40% in 2018. Instead, bonus depreciation actually increased to 100%.

Perhaps even more exciting than the increase is the inclusion of used equipment. Previously, new and used equipment was eligible for Section 179, but bonus depreciation was reserved for only new equipment. Now, used equipment that is purchased or financed during the tax year can qualify for 100% bonus depreciation.

How It Works

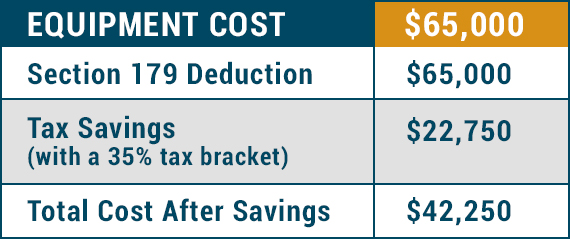

When you finance equipment for your business, Section 179 allows you to write off the entire purchase price of the equipment that year rather than using normal depreciation to spread it out over the course of the useful life of the asset. Take a look at this example:

Bonus depreciation comes into play when the equipment starts to exceed the Section 179 limit. For example, if you finance equipment costing $1.5 million dollars, one million of that will be deducted through Section 179. The remaining $500,000 is then eligible for 100% bonus depreciation.

What It Means for You

As a small business owner, these changes make 2018 a great year to expand with equipment. The increased limits and inclusion of used equipment mean most businesses will be able to benefit. By combining the Section 179 tax benefits with financing, equipment can more easily fit into your 2018 budget. To see what your tax savings could be, check out our calculator.