You’re finally ready to buy your dream home.

Your income looks good. Your credit score checks out. Everything is lined up.

Then the bank delivers the bad news: “Sorry, but you’re too leveraged.”

How did that happen?

In many cases, it comes down to one decision: Using personal credit to buy hardscaping equipment, like skid steers, mini excavators, wood chippers, landscaping trucks, and more. That single choice can cost you your mortgage approval, even if your business is doing well.

Hardscape Mentor teamed up with Beacon Funding to help contractors grow without sacrificing their personal goals. One question we hear newer business owners ask all the time:

Why shouldn’t I use my personal credit to buy hardscaping equipment?

In this article…

- How Personal Credit Is Really Reviewed

- The Mortgage Math That Changes Everything

- The Hidden Danger of Using Home Equity

- The Smarter Way to Finance Equipment

- Protect Your Business and Your Personal Goals

- Free Guide: Scale Like a Pro with Beacon Funding’s 9 Tips for Hardscapers

- Frequently Asked Questions

How Personal Credit Is Really Reviewed

When you apply for a mortgage, an auto loan, or even certain credit cards, lenders look at more than just your credit score.

They also evaluate how leveraged you are: meaning how much debt you’re carrying every month.

If your credit cards are maxed out, you have an auto loan, and now you’ve added an equipment payment on your personal credit, lenders see you as highly leveraged.

Even if your business is making the payments, that debt still shows up on your credit report as your personal obligation. It’s not just about what makes sense to you, it’s about how it looks on paper.

And the more leveraged you appear, the more your borrowing ability shrinks. In some cases, high leverage can even lower your credit score, making it harder to qualify for major personal purchases.

To understand how quickly personal credit can hurt you, let’s look at a simple example.

The Mortgage Math That Changes Everything

Let’s say you take home $5,000 per month in personal income. After your auto loan ($700) and credit cards payment ($700), you have about $3,600 left in remaining income.

But that doesn’t mean lenders will approve you for a $3,600 mortgage payment. Lenders want to make sure you have enough of your remaining income to afford basic living expenses, like groceries, utilities, etc.

Instead, when you apply for a mortgage, the lender uses your fixed expenses and monthly income to calculate your debt-to-income ratio (DTI). They’re trying to look at your fixed expenses compared to what you bring home every month.

How do they do this? They divide your fixed payments by your monthly income to figure out your debt-to-income ratio.

$1,400

FIXED PAYMENTS |

28%

DEBT TO INCOME RATIO |

$5,000

MONTHLY INCOME |

Lenders use your debt-to-income ratio to check how much you can pay each month for your mortgage. This helps them make sure you’ll still have enough money left over for everyday living expenses, so your personal finances aren’t stretched too thin.

If your debt-to-income ratio is too high, it shows lenders that you’re already using a large portion of your monthly income to pay off existing personal debts. This means you may not have enough financial flexibility to safely take on a mortgage, making it less likely you’ll be approved.

Now if you add an equipment financing payment ($850 for a new skid steer, for example) to your personal credit, your debt-to-income ratio rises, your remaining income drops, and so does your borrowing power.

-$850

EQUIPMENT PAYMENT |

$1,650

REMAINING INCOME |

-$700

CAR PAYMENT |

-$700

CREDIT CARD PAYMENT |

-$1,100

MORTGAGE PAYMENT |

Basically, a lender will not want to approve you for a mortgage payment ($1,100) because they feel like it’s going to put too much undue stress on your personal expenses.

The takeaway: Adding an equipment financing payment to your personal credit extremely limits your borrowing power.

The Hidden Danger of Using Home Equity

What about using a home equity loan? Some contractors consider using a home equity loan, and on the surface it might seem convenient, but it’s even riskier.

Why is it riskier? When you use home equity, you’re tying your house to your business.

If your hardscaping business hits a slow season or cash flow tightens, you’re not just risking equipment but you’re risking your home too. Business setbacks can suddenly turn into personal emergencies.

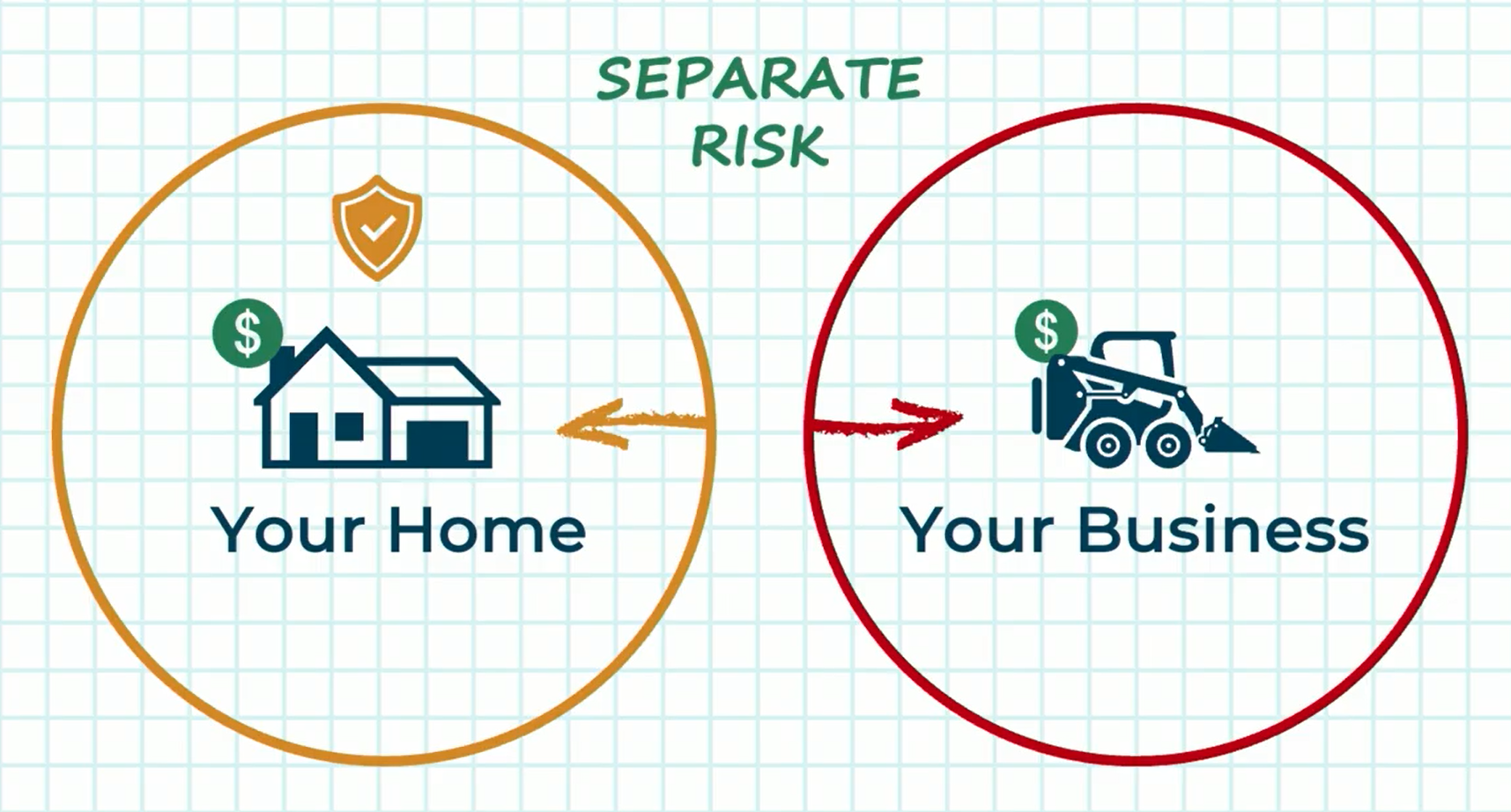

To protect yourself, finance hardscaping equipment through your business. This avoids risk by keeping debt where it belongs: with the business, not your personal life.

Why Mixing Personal and Business Debt Is a Problem

When business debt lives on your personal credit, it creates long-term challenges:

- Your personal credit score can suffer

- Mortgage and auto loan approvals become harder

- Your personal financial flexibility disappears

Hardscape Mentor and Beacon Funding are here to help your business grow the right way… and that starts with separating business and personal finances when adding equipment into your hardscaping business.

The Smarter Way to Finance Equipment

So, what’s the better option? That’s where Beacon Funding comes in.

Beacon Funding offers business loans specifically designed for equipment purchases. When you finance through Beacon Funding, the loan is tied to your company, not your personal credit profile.

That separation matters.

By financing equipment through your business:

- The debt stays under your company’s name

- Your personal borrowing power stays intact

- Your mortgage goals remain protected

- Your personal finances – and even your home – are shielded from business risk

Instead of hurting your future, your equipment investment supports it.

Protect Your Business and Your Personal Goals

You’re not just buying a skid steer, mini excavator, landscaping truck, or any other hardscaping equipment… you’re building a business and planning a life outside of it.

When equipment debt sits on your personal credit, it can quietly block the milestones you’re working toward. Business-first financing helps you grow without putting those goals at risk.

Free Guide: Scale Like a Pro with Beacon Funding’s 9 Tips for Hardscapers

If you’re wondering how to finance hardscaping equipment the right way, Beacon Funding have bundled everything into one powerful resource.

Download Beacon Funding’s free guide, Scale Like a Pro: 9 Tips for Hardscapers, to access proven smart strategies for contractors like you looking to expand smarter, not riskier.

Inside the guide, you’ll learn how to:

- Use equipment financing as a growth tool

- Manage cash flow while adding profit-producing equipment

- Make confident decisions that supports long-term business growth

CLAIM YOUR FREE GUIDE

Inside the guide, you’ll also learn about exclusive VIP perks, including:

- $0 down financing

- 90 days with no payments

- VISA gift cards

If you’re ready to grow your business without sacrificing your personal future, Beacon Funding and Hardscape Mentor are here to help.

Frequently Asked Questions

Why shouldn’t I use my personal credit to buy business equipment?

Using personal credit for business equipment increases your personal debt and makes you look more “leveraged” to lenders. Even if your business makes the payments, that debt still counts against you personally. This can limit your ability to qualify for major life purchases like a mortgage or auto loan.

How does personal equipment debt affect my ability to buy a home?

Mortgage lenders look closely at your debt-to-income ratio (DTI), not just your credit score. When an equipment payment sits on your personal credit, it raises your monthly obligations and reduces how much mortgage lenders are willing to approve, sometimes enough to stop a home purchase altogether.

What’s the safer way to finance business equipment?

The smarter option is to finance equipment through your business instead of your personal credit. Business-first equipment financing keeps the debt under your company’s name, protects your personal borrowing power, and helps you grow without putting your home or financial goals at risk.